My Social Security Benefit Statement on Public Display

In this post, I show you my actual Social Security Benefit statement. Most people never look at their own or don't have sufficient basic math skills to understand it. I will dissect my own statement for you and you will then understand how Social Security works better than 99.9% of the population. Sadly, the people who understand it least are those receiving benefits. I find that many of these people would rather have their opinions than make the effort to learn what is true.

I have attached my Social Security benefit statement from the Social Security Administration. You can get a copy of your benefit statement @SSA.gov. We need three pieces of information to show where the money comes from to pay those monthly checks to seniors.

Two pieces of information we need are on the Social Security benefit statement.

Most people think that they get the largest payment automatically. Not true. You need to make choices when you apply and if you make the incorrect choice, you get a smaller check -- for life. Even if you already receive Social Security Benefits, you may be able to change your selections.

The statement shows how much I have already paid in and it shows how much I will be receiving when I begin my Social Security benefits. The third piece of information we need, the only estimate required, is how much more I will pay in to Social Security between now and the time I start my benefits. I can make this estimate with a great degree of accuracy because the percentage of my pay that is taken to fund my Social Security benefits is published by Social Security at http://www.ssa.gov/OACT/COLA/cbb.html#Series

Social Security estimates that I will earn $57,298 for each of the next 6 years (see above graphic). From this amount, 12.4% or $7105 will be contributed annually to my Social Security account. Note--since I am self employed, I pay BOTH portions as the government treats me as the employee and the employer.

Now we have the three pieces of data we need.

1. amounts I and "my employer" have paid in per the benefit statement = $231,853

2. amounts I and my employer will contribute over the next 6 years = $42,629 (6 years x $7105 annually)

3. amount that I will receive monthly for life (let's assume no adjustment for inflation) per the benefit statement = $1794 monthly starting at age 62

Let's see how fast I get "paid back" by dividing the monthly amount I will get at age 62 into the amounts I will have paid in:

Amounts paid in at age 62 by me and my employer= $274,482 (items 1 and 2 above)

Divided by my monthly benefit $1794

=153 months it takes for my "account" to run out.

Let's round up and call that 13 years. So to age 75, the benefits I get are paid for by my own (and employer's) contributions. But what if I live beyond age 75? Where does my $1794 per month come from? It comes DIRECTLY OUT OF THE PAYCHECK OF YOUR CHILDREN AND GRANDCHILDREN WHO WILL BE WORKING.

SEEM FAIR?

You may remember that Rick Perry who was a candidate for the Republican nomination for president was quickly forced to end his candidacy after he made the statement that Social Security was a Ponzi scheme. In politics, the worst thing one can do is tell the truth. People don't want to hear the truth, they want to hear what they already believe. And beliefs, more times than not, have nothing to do with facts.

Here's the definition of Ponzi scheme from Wikipedia:

A Ponzi scheme is a fraudulent investment operation that pays returns to its investors from their own money or the money paid by subsequent investors, rather than from profit earned by the individual or organization running the operation. The Ponzi scheme usually entices new investors by offering higher returns than other investments, in the form of short-term returns that are either abnormally high or unusually consistent. Perpetuation of the high returns requires an ever-increasing flow of money from new investors to keep the scheme going.

The above is an accurate description of Social Security because it returns to investors their own money or the money paid by subsequent investors.

Just substitute the word taxpayer for investors and the above sentence is 100% accurate regarding Social Security.

So I want to clearly show to you that Social Security is a Ponzi scheme and that most seniors who think that they merely get back what they paid into the system are sorely mistaken. In fact, even some of those who read this post will continue to believe that they are owed or due this money when in fact this is their opinion, not based in fact.

If that is not a Ponzi scheme where the "early" investors are paid off by money of later investors, I don't know what would qualify.

But the situation is much worse than the above scenario for the following reasons:

1. the number of people receiving social security benefits increases by 37,000 a month (I compared 12/2009 thru 10/2012)

2. notice on my benefit statements that if things are really bad, my family can collect as much as $4,360 per month. So if retirees don't do enough individually to drain the system, plenty of family members will join in

So there you have it. An actual look at a benefit statement so you can see that amounts paid to retirees, while some of the money they paid in, is an entitlement--a direct tax on the younger workers transferred to the bank account of the retirees. As for talk of saving the system, Madoff tried to save his Ponzi scheme and you see the result. Ponzi schemes are doomed for failure and cannot be saved. While you may not like this post or the facts, these are facts and not opinions.

And once we all agree on the facts, we come much closer to solving a problem.

Social Security cannot be "fixed" just like a Ponzi scheme cannot be fixed. If we want to tax the productive members of society (those working) and give that money to those who are now unproductive (i.e. not working), then let's call it that and see if we all vote for that. But let's just tell the truth.

A better solution would be to stop this nonsense by paying out whatever there is in the Social Security pot as long as it lasts to all those currently retired and do away with it. We could then go back to a system that works--people save for themselves rather than being a burden on others who are forced to hand over their hard-earned money.

Your opinion facts?

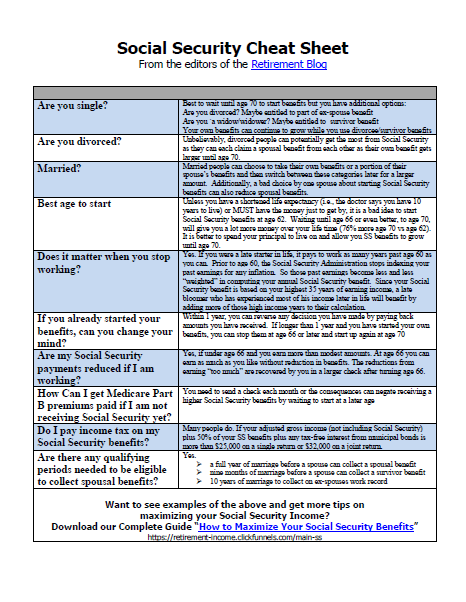

Maximize Your Social Security Income

Get the one-page social security Cheat Sheet

You may think that the folks at the Social Security office will tell you how to get the biggest monthly check. In fact, the federal rules PREVENT them from advising you. There are millions of people who have given up more than $50,000 just by making a simple yet incorrect method of taking their Social Security benefits. Don’t let that be you! Get your free copy now.

Well now this is some important information. Thanks a lot for investing your time and effort to share it with us.

so love this post im impress thank qqq

this is real good post i like it thank q

Social Security Benefit Statement and See How Social Security Benefits to us. Social Security is very important.

I’ll keep updating and adding to this DoFollow blogs list. As I mentioned above, feel free to let me know of any blogs (including your own) that would be a good fit here.

this blog is very informative about social securities.

This information was very interesting as well as the solution. Thank you for sharing your wisdom with us!